Trust Tuesday: Investment Update | June 2021

By: Caley Perleberg, CFA, AVP Trust Portfolio Manager I

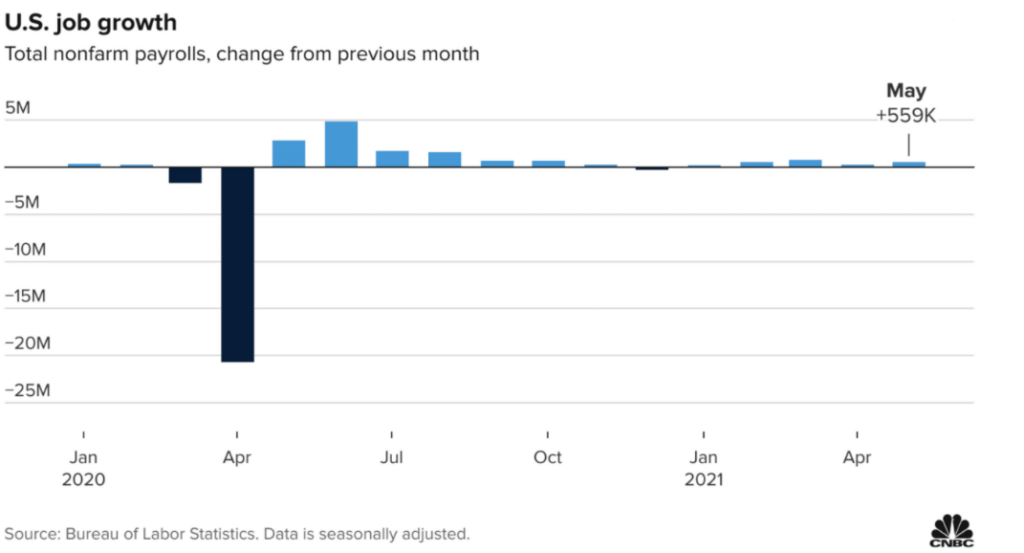

Jobs OK in May

The May U.S. Jobs Report was a case of good news, the bad news:

- The U.S. added 559,000 jobs in May, missing expectations of 671,000

- The markets viewed the miss as a positive turn of events. A blowout number may have prompted the Federal Reserve to start considering reducing some of its simulative measures

- The unemployment rate fell from 6.1% to 5.8%

Inflation Nation?

“There are two camps on inflation. One believes it will be transitory in nature, while the other expects it to persist.”

With inflation concerns, one of the main topics of 2021 (and rightfully so) let’s first look at the two gauges of inflation here in the U.S. The Consumer Price Index (CPI) and the Personal Consumption Expenditures (PCE). We won’t get into all the details of each, but the CPI is the inflation we as consumers can relate to. When setting policy (think short-term interest rates) the Federal Reserve uses PCE. Each inflation reading has different weights, but two of the main differences between are:

- CPI tends to be less volatile as it strips out energy and food

- PCE is broader in its scope as it takes into account goods of both consumers and businesses (CPI only accounts for consumers)

While inflationary concerns are warranted (the biggest risk to any investor is the erosion of their purchasing power), long-term demographic trends and technology should keep runaway inflation at bay.

Going Forward

- The U.S. economic reopening is fully underway as vaccinations are providing increased confidence and driving consumer spending.

- Unfortunately, many countries are still dealing with rising cases and lockdowns. Eventually, they will begin to recover and fully open.

- While job growth has missed expectations the past few months, we expect growth to continue and the unemployment rate to fall.

- With pockets of inflation running hot, the Federal Reserve must navigate and communicate effectively. This is our paramount concern and the biggest risk to the markets